14 Reasons why the Informal Credit Market is used by the Poor: Policy Implications for Microcredit Programmes in Developing Countries

IntroductionMany developing countries, despite double digit growth rates, have lagged far behind in terms of quality of living in urban areas. Problems of unemployment, inadequate housing, poor environmental quality, rampant crime, poverty, transportation etc. have plagued urban residents and decision makers alike. While the attempts of governmental agencies have been commendable, shear scale of the problem has diluted such efforts, resulting in the benefits being spread thinly among a large population, or not benefiting most of them. Low income households in developing countries are seen as particularly vulnerable. Their personal problems of low education and skill levels, low incomes, lack of marketable assets, and uncertain job markets have been compounded by external factors that have failed to provide adequate infrastructure and social services that would have enabled them to participate in mainstream economic activities. As a result, this has affected every facet of their life: employment (predominantly in the informal sector), education (non-existent or up to primary levels only), health (low quality or traditional), housing (impermanent materials and illegal settlements) etc. Often the problems of low-income households can be traced back to a single factor which, on a cumulative basis, has affected other factors, resulting in their present condition. For low income households, one such cumulating factor is credit, or the lack of access to adequate bank credit. This lack of access has resulted in households turning to informal credit markets (ICMs) to satisfy their need, where elaborate networks of credit delivery have been set up by different kinds of informal suppliers. Examples include money lenders, pawn brokers, ROSCAs, credit societies/unions etc. With governmental action in ensuring an enabling policy/programme environment not forthcoming or insufficient, particularly with innovative financing mechanisms, there is a need to understand the systems of credit delivery that the low-income households themselves have established to fill the gap. This financial dualism of "formal" and "informal" is a result of both the shortcomings of the formal sector and the intrinsic condition and position of the urban low income households themselves [Germidis et al., 1991]. Delivery of credit for various purposes should be ensured not only by increased financial services of banks and other financial institutions, but more importantly, by also taking into account the existing systems of credit delivery already in place in the settlements. This calls for a better understanding of the systems of credit developed by the urban low income households, the advantages it offers, and implications of such systems for devising appropriate microcredit programmes for their needs. The material presented in this paper is part of a larger survey of low-income households and informal credit suppliers carried out in April-June 1995 in Bangalore, India [Srinivas, 1996]. Information gleaned from interviews with settlements leaders, NGOs, traders and shopkeepers, social workers etc. was also used to substantiate the data collected. The ICM is vast, covering different types of suppliers providing credit for different purposes. However, the survey was limited to credit activities that were taking place within a settlement or community that serviced low-income households.

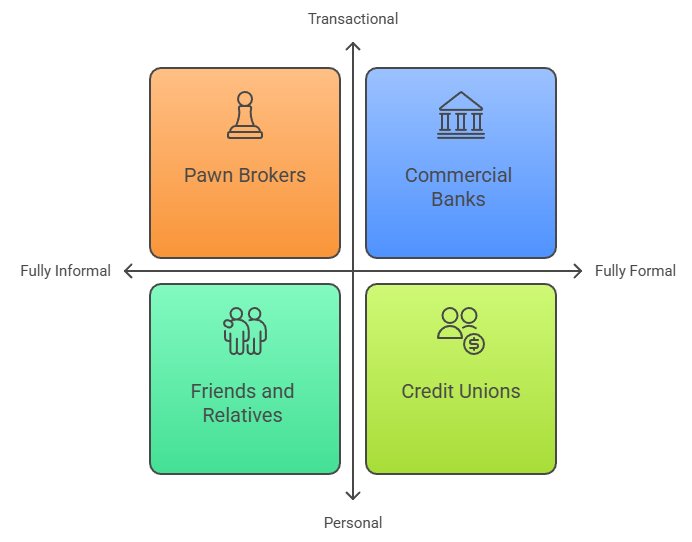

What is informal credit?The line dividing "informal" credit and "formal" credit is very fine, and credit suppliers on both sides actually form a continuum that range from very informal suppliers (like friends, relatives neighbours etc.) to fully formal suppliers (banks and specialized financial institutions). Ranged in between these extremes are rotating savings and credit associations (ROSCAs), money lenders, pawn brokers, credit societies, traders etc. [Srinivas and Higuchi, 1996]. They mobilize savings and provide credit, or as in the case of ROSCAs, do both. The ICM is highly heterogenous in nature. It encompasses short term flows in funds markets, lending and borrowing of small amounts among group members, friends or relatives. It includes activities of finance companies, as well as those of pawnshops and money lenders. It runs the gamut from large wholesale traders financing trade, to village level crop buyers, to petty shopkeepers and itinerant peddlers. It also includes organized credit unions, ROSCAs (called 'chit funds' in southern India), credit societies etc. With advantages of unregulated money supply, easy accessibility, easy liquidity, low 'administrative' and procedural costs, little or no collateral/mortgage requirements, flexibility in interest rates and repayment schedules, ICMs are ideally suited to cater to the lower income groups [ADB, 1990]. Three types of informal credit suppliers can be observed in the ICM. The "transactional" credit suppliersCthose for whom credit is a business transaction. Examples include, pawn brokers, money lenders, traders, employers etc. The "mutual" credit suppliers - those for whom credit supply is a give and take process. Examples include, chit funds/ROSCAs, credit unions, credit societies, people's organizations/self help groups. The "personal" credit suppliers - those for whom credit supply is a private arrangement that may be reciprocated in the future. Examples include friends, relatives, co workers and neighbours [Srinivas and Igel, 1995]. Ranged along with formal commercial banks and financial institutions, transactional, mutual and personal suppliers would form a continuum. This would enable the positioning of 'fully informal' personal suppliers and the 'fully formal' banks at either end of the continuum, with the 'semi-formal' and 'semi-informal' transactional and mutual suppliers in between [Srinivas and Higuchi, 1996]. (While the definition of an NGO is broad and covers a range of organizations and institutions, it was not included here since it was observed that NGOs primarily function as catalysts, intermediaries and facilitators - aiming for a greater degree of community managed microcredit programmes).

Figure 1: A continuum of informality in the credit markets A common thread that runs through all of them is their informality, adaptability and flexibility of operations - features that reduce their transaction costs and confers upon them their comparative advantage [Ghate, 1990]. The following aspects characterize the ICM:

Credit Demand and Supply in the Informal SectorStringent requirements for loans have systematically kept low income households out of the credit delivery network of commercial banks. Bank managers interviewed during field research revealed that banks required borrowers to have a job in the formal sector, with "steady" employment and an incomes at "adequate" levels, whereas most of the households surveyed had informal sector jobs (83.7 percent) or transient jobs in construction sites. This kept their incomes very irregular and uncertain. Banks required that only borrowers with valid land ownership or ownership certificates were to be eligible for loans but most of the low income households lived as squatters and did not own the land (100 percent of the sample). Banks requested collateral for loans, usually in the form of marketable assets, for example, the house to be built or the land itself. Mean household income of the samples studied was about Rs. 1000 per month (Rs. 40 = US$ 1, 1991). They owned very few assets, and their savings by themselves was insufficient to act as a collateral. Most bank loans were large, for lump-sum/one-time investments, whereas the surveyed households usually staggered expenditures over a period of five to eight years. Such conditions invariably led urban low income households to depend on ICMs to satisfy their credit needs. In the informal sector, income levels, land ownership and job status were not important for obtaining loans from the ICM. Loans were made on a face to face basis with personal knowledge and close proximity of the lenders and borrowers. Practically no collateral was demanded during such transactions (except, of course, in the case of pawn brokers, who lent amounts based on the value of items pawned by the borrower). Close acquaintance between the lender and borrower also ensured that loans were available quickly without any need for elaborate paperwork and costing little in terms of administration and information. Most of the loans were small, to finance only a particular part or fraction of the overall investment process. Expenditures were staggered and spread over a long period of time (from five to eight years) so that burdens of immediate loan repayment or interest payments were low and repaid quickly (less than eight weeks). By providing loans of small size (Rs. 2,000 to Rs.5,000), informal suppliers satisfied their credit needs. Besides, the long held belief of usurious practices in ICM can be put to question since, despite "high interest rates" on an annual basis, actual interest payment burdens are low, since loans are small in size and are repaid in a very short period. Informal suppliers interviewed in the study did not receive any support from the government or financial institutions. They used their own resources and profits generated by increased circulation of loan funds (for money lenders, pawn brokers, employers) or used the savings of group members to lend (ROSCAs, credit societies etc.). Since their funds were not insured or were not secured by collateral in any way, risk of default was high. But close links and personal relationships were maintained between borrower and lender. This meant that there were few defaulting borrowers observed in the study (less than 2.3 percent of borrowers). Dispensing with the elaborate requirements and paperwork of conventional banking, informal suppliers have devised their own methodologies which have worked to suit the conditions and positions of its low income clientele. Small scales of operation mean that informal suppliers function without the inter and intra agency support typical of formal financial institutions. However, a fundamental disadvantage of informal credit observed was that large capital investments or other such lump-sum investments were difficult to be made, affecting as a result, expansion of production, higher income generation or quality/quantity improvement.

Official approaches to informal creditThe attitudes of the government towards the ICM have ranged from the negative, by attempting to curb its functions, to the positive, by duplicating the relative organizational and operational advantages that ICM offers to low income households. NGOs and community groups have also been used, in some cases, as intermediaries to channel credit to low-income households. Initial approaches of government agencies have attempted to curb the activities of ICM suppliers on the justification that it affected the smooth functioning of economic, monetary and financial policies, and encouraged the circulation of illegal or "black" money. Extensive legislation, rules and regulations have attempted either to restrict its functioning, or effect outright termination of their activities. To counter ICM operations, monetary authorities have also called for increased banking activities and better networks of credit delivery that met not only economic goals, but also social and developmental goals. An example of this is the "Priority Lending Areas" established by India's central bank, the Reserve Bank of India. This stipulates that 25 percent of all lending of a bank should be towards "weaker" sections of the society. ICM practices have also been adopted by some commercial banks. The Syndicate Bank launched its "Pygmy Scheme" where authorized commission agents went from door to door daily, collecting small amounts of money as savings from households and businesses. Recently, the Vijaya Bank has been working with NGOs to channel credit to very low-income households. A gradual shift of attitudes from negative to positive can be seen in the call for integration of informal and formal credit sectors by financial experts and monetary authorities [ADB 1990, Germidis 1991, de Groot 1988, Gupta 1987, Kropp 1989, NBARD 1992 and Nanda 1994]. The strategy of integration envisages the absorption of the informal sector into the formal sector by integration and institutionalization. But this approach has been challenged with the belief that the informal sector by itself plays a beneficial role in overall economic growth, and therefore the two sectors should in fact be linked and should complement each other, without destroying the essential informality of the ICM. [Germidis, 1991]. Such an approach calls for a better understanding of the way in which the ICM functions and the relative advantages that it offers over formal credit. Why do low income households use informal credit for their investment needs? Is it a negative match (because they are not eligible for formal credit), or is it a positive match (because informal credit is a viable choice for their socio economic condition and position)? Or is it a combination of both? This would help in developing support policies for the ICM, and ultimately its smooth linkage with the formal sector.

Fourteen reasons why the poor use the informal credit marketThis paper attempts to highlight the positive aspects of the match between informal credit and low income households, and to draw lessons and good practices in the organizational and operational set up for designing microcredit programmes. It would be imprudent on the part of monetary authorities and economic planners to ignore the vast credit delivery networks already in place serving the low income households. A middle ground has to be found, where the advantages of ICMs are built upon (and disadvantages minimized), and a change in attitude of formal institutions towards the ICMs' activities brought about, so that linking the two sectors will be smooth and would increase credit availability. As mentioned earlier, the first step to be taken is a deeper and broader understanding of the ICM. There are essentially 14 reasons why ICMs are used by the urban poor. Many features are clearly interlinked, and collectively influence the effectiveness of ICMs.

Implications for Microcredit ProgrammesThe market structure of informal credit supply and demand provides valuable insight for the designing of effective microcredit programmes targeted at low income households. Three key lessons emerge from the 14 reasons mentioned above. Firstly, due to localized services, specific borrowers, personalized services and close informational links, credit supplied by the ICM is timely. Credit is made available when it is most needed and with the shortest possible transaction time. Prompt response is possible also due to proximate physical/psychological links that lenders maintain with their borrowers. Therefore, microcredit programmes should incorporate strong information links, close physical proximity to borrowers, and develop information campaigns in its organizational framework. Operationally, less procedure and paper work in establishing the borrowers' credit rating, and office timings that are flexible and integrated into the work cycles of the borrowers, should also be included. Secondly, strong organizational structures, non profit motives, opportunities for very small savings and other features encourage borrowers to save. Many credit groups provide loans only if a specified amount is saved by the member/borrower. Microcredit programmes should mirror this, by linking loans and amount saved. For example, loans can be a multiple of the amount saved. Information links and screening of members for commitment and collateral should also be done for efficient implementation and repayment behaviour. Besides, a dynamic network within the settlement to mobilize savings, programmes that enforce savings, or encourage savings, should be incorporated in its operations. Thirdly, the terms and conditions of loans made by informal suppliers are very flexible. These are worked out on a mutually agreed formula, and even within a credit cycle, it can be modified to suit the changing socio economic status of the borrower (A typical modified loan criteria, for example, was the frequency and time of repayments). This calls for microcredit programmes that develops cohesiveness and carries out group activities, binding its members together. It should also tailor loan terms and conditions to meet specific needs and requirements of borrowers. Terms and conditions of the credit programme should also be easily understood, with implied trust between the parties involved. The viability of informal credit has to be understood in terms of the positive match between informal suppliers and low income borrowers. The objective of this paper has been to highlight the positive features of ICMs that enable it to effectively reach the low-income households. While not advocating the absorption of these informal operations into mainstream or formal financial initiatives, the paper presents a case for adopting the positive features and methodologies into microcredit programmes developed by NGOs or commercial banks (see Table 1 for a summary of the discussion, as well as some of the drawbacks of adapting ICM features). Further research is indeed necessary in understanding adaptability of ICM features into mainstream microcredit programmes, as well as other factors that effect such programmes. Of particular significance for study is the role of NGOs, both local and international, as intermediaries and animators in developing microcredit programmes for low-income households. NGOs have greater flexibility and adaptability in developing their programmes. The process of NGO intervention into low-income communities on one hand, and the adoption and incorporation of positive ICM features into microcredit programmes needs further study.

References:

Hari Srinivas - [email protected] |