Economic Instruments for Environmental Policy: Solving global environmental problems with local economic action

Hari Srinivas

Policy Analysis Series E-190.

Abstract:

The article explores the use of economic instruments for sustainable business specifically how economic instruments, such as taxes, subsidies, and market-based mechanisms, can be used to encourage sustainable business practices. The article highlights the benefits of using economic instruments, such as cost savings, improved resource efficiency, and reduced environmental impact.

The article also discusses some of the challenges associated with the implementation of economic instruments, such as the need for political will, the need for effective implementation, and the need for public understanding and support. The article concludes by emphasizing the importance of economic instruments as a tool for promoting sustainable business practices and contributing to sustainable development.

Economic instruments (EIs) are tools that governments and businesses can use to influence economic behavior. Examples of EIs include taxes, subsidies, and regulations. These tools can be used to encourage or discourage certain activities, such as the consumption of certain goods or the use of certain resources. EIs are often used as part of a larger economic policy, and can be a effective way of achieving specific policy goals.

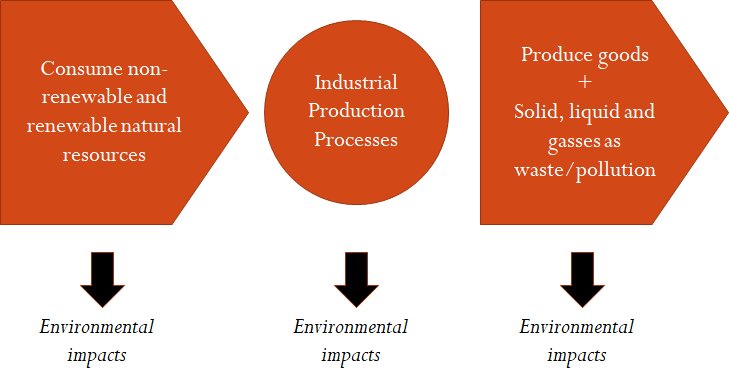

Figure 1: Environmental Impacts of Production Processes

Economic "carrot-and-stick" approaches are necessary, considering the complex nature of production processes that provide goods and services (Figure 1), and the environmental impacts that each stage of the production process generates. This can be solid wastes and residue, but also liquid wastes, waste water, as well as gaseous pollution and GHG emissions.

EIs help in tackling these myriad of impacts using fiscal and other economic incentives and disincentives. Such instruments help incorporate environmental costs and benefits into the budgets of households and enterprises.

The objective of economic instruments is to encourage environmentally sound and efficient production and consumption through full-cost pricing. EIs include effluent taxes or charges on pollutants and waste, deposit-refund systems and tradable pollution permits.

- OECD

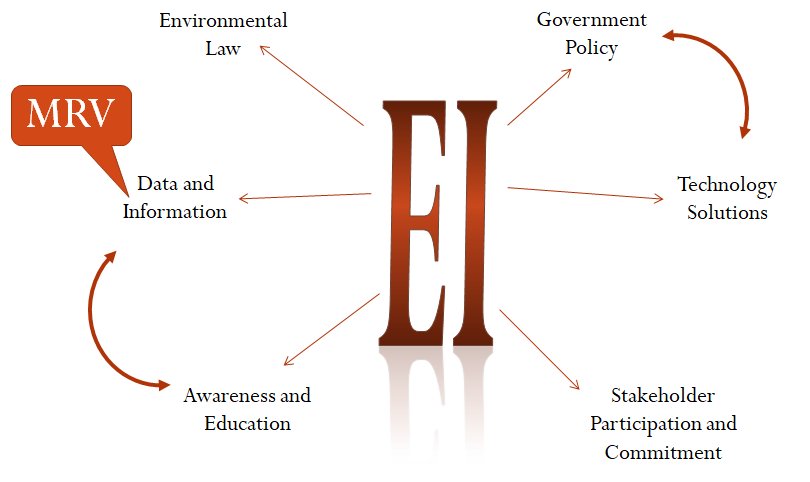

Figure 2: Key Aspects of EIs

* MRV = Monitoring, Reporting and Verification

EIs are not just money-denominated policies, but also include a number of other key aspects (Figure 2) - much of which are required to determine the size of the EIs to be implemented as well as incentives to promote action and verification.

Such an "ecosystem" of aspects include, for example, data and information (and including their monitoring, reporting and verification), environmental laws, government policies, technology solutions, stakeholder participation and commitment, awareness and education, etc.

EIs, such as levies/charges and tradeable permits, when used appropriately can provide least-cost solutions to environmental problems, provide greater flexibility and encourage innovation. EIs can be used on their own or in combination with other measures to improve the efficiency of environmental protection efforts

Although economic instruments are often associated with government policy, many are encountered in everyday life. The examples below illustrate how these instruments influence the choices made by households, businesses and communities.

Table 1: Economic Instruments in Everyday Life

Economic Instrument

Everyday Example

Tax

Carbon tax on fossil fuels encourages energy conservation and cleaner alternatives.

Subsidy

Government grants or rebates help households install rooftop solar panels.

User Fee

Pay-as-you-throw garbage collection charges encourage waste reduction and recycling.

Deposit-Refund System

A refundable deposit is paid when purchasing bottles or cans and returned upon recycling.

Tradable Permit

Companies buy and sell carbon emission allowances under emissions trading schemes.

Liability Rule

Businesses responsible for pollution must pay for environmental cleanup and restoration.

Performance Bond

Mining companies deposit funds that are refunded only after successful site rehabilitation.

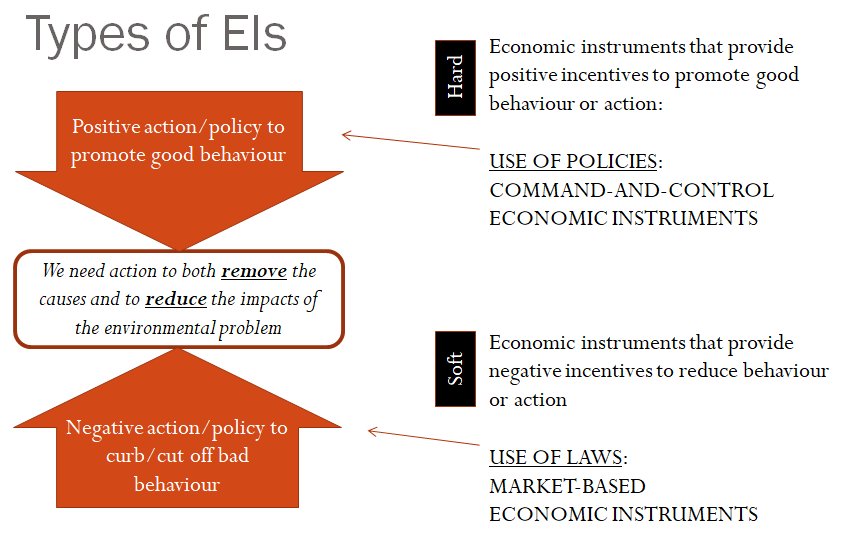

For EIs to be effective we need action to both remove cases of environmental problems and reduce the impacts of such problems (Figure 3). This can include EIs that provide positive incentives to promote good behaviour and action - policies and EIs that are essentially market-based. Conversely, it can also include EIs that provide negative disincentives to reduce or eliminate behaviour patterns or action that are harmful to the environment - policies and EIs that are essentially of the "command-and-control" type..

Some examples of EIs include taxes, subsidies, tariffs, and quotas.

Taxes are charges levied by governments on goods, services, income, or wealth. They can be used to raise revenue for the government, but they can also be used to influence behavior. For example, a government might impose a high tax on cigarettes to discourage smoking, or a tax on carbon emissions to discourage the use of fossil fuels.

Subsidies are payments made by governments to businesses or individuals to encourage certain behaviors. For example, a government might provide subsidies to farmers to encourage them to grow certain crops, or to homeowners to encourage them to install solar panels.

Tariffs are taxes on imported goods. They are often used to protect domestic industries from foreign competition, or to raise revenue for the government. For example, a government might impose a tariff on imported cars to protect the domestic auto industry, or a tariff on imported steel to raise revenue.

Quotas are limits on the quantity of a good that can be imported or produced. They are often used to protect domestic industries from foreign competition, or to conserve natural resources. For example, a government might impose a quota on the amount of fish that can be caught to protect fish stocks, or a quota on the amount of oil that can be imported to reduce dependence on foreign oil.

Figure 4: EIs' Target for Action

EIs' targets for action (Figure 4) focus on the entire lifecycle of a product or service - in its production and consumption processes - ensuring that both stationary sources of pollution (i.e. pollution from factories, businesses and homes etc.), as well as mobile sources of pollution (i.e. pollution from transportation - all types of vehicles) are targeted by the EIs.

Table 2: Environmental EIs

POLLUTION CHARGES

Charges on pollutants discharged in to the atmosphere, water bodies and surface from the stationary sources

Charges on the pollutants discharged from the mobile sources, (charge is set on the fuel used)

Product charges on goods (tires, lamps, filters, batteries) harmful to the environment

Why do we need EIs? Global environmental problems (Figure 5) such as climate change of loss of biodiversity have (1) a number of causes - direct and indirect, and also have (2) a number of impacts - short-term and long-term. In such a situation, EIs are used by governments to influence economic activity and tackle environmental challenges.

Figure 5: Why do we need EIs?

Some common reasons for using EIs include:

Raising revenue: Governments use taxes and other EIs to raise money to fund public services and infrastructure.

Encouraging or discouraging certain behaviors: EIs can be used to encourage or discourage certain behaviors, such as consumption, production, or investment. For example, a government might use subsidies to encourage the production of renewable energy, or impose a tax on cigarettes to discourage smoking.

Protecting domestic industries: EIs, such as tariffs and quotas, can be used to protect domestic industries from foreign competition. This can help to preserve jobs and support the domestic economy.

Reducing negative externalities: EIs can be used to address negative externalities, which are costs or negative effects of economic activities that are not reflected in market prices. For example, a government might impose a tax on carbon emissions to discourage the use of fossil fuels, which can help to reduce air pollution.

Figure 6: Environmental Policy and EIs

As outlined in Figure 5, the action to remove the causes and to reduce the imacts of environmental problems necessitates the use of money and finance as key policy tools to change behavior - either good or bad.

Purposes of EIs

To reduce the pollution in to the atmosphere from the stationary and mobile sources

To reduce waste generating and to provide incentives to producers and importers invest in to the waste recycling measures.

To create incentives for users to use more friendly goods and products

Challenges for EIs

With cost savings a major financial objective for households and businesses alike (besides profit-making for businesses), avoiding costs due to environmental impacts can be a key incentive to take environmental action at the local level. EIs can help in reinforcing positive behavior, while curbing behaviours that have negative impacts on the environment.

Challenges to the effective use of EIs remain. These include the issue of Monitoring,-Reporting-Verification (MRV) to ensure that decision-making related to EIs are grounded in reliable, accurate and timely information. EIs also need consistent commitment and action from all stakeholders - governments, business and industry, and the civil society - targeted at both production and consumption processes.

While a range of actions are needed at the local level to solve the myriad of problems we face, EIs provide a basket of solutions for action to be taken - targeting everyday decisions and consumption/production patterns.

Local communities were granted legal rights to manage nearby forests. Because villagers directly benefited from sustainable harvesting, forest cover improved while local incomes increased. The assignment of clear property rights created incentives for long-term resource stewardship.

Why it works: Demonstrates how ownership and management rights can reduce environmental degradation.

2. Market Creation

Carbon Emissions Trading in the European Union

The European Union Emissions Trading System created a market for carbon allowances. Companies that reduce emissions below their limit can sell surplus permits to firms that exceed theirs.

Why it works: Illustrates how governments can create entirely new markets for environmental goods and services.

3. Fiscal Instruments (Taxes and Subsidies)

Sweden's Carbon Tax

Introduced in 1991, Sweden imposed a tax on fossil fuel carbon emissions. The tax encouraged energy efficiency and a shift toward renewable energy while maintaining economic growth.

Example: Germany's Solar Subsidies

Government subsidies and feed-in tariffs helped households and businesses install solar photovoltaic systems, accelerating renewable energy adoption.

Why it works: Shows both the "stick" (tax) and the "carrot" (subsidy).

4. Charge Systems (Fines and Fees)

Pay-As-You-Throw Waste Collection in Japan

Many Japanese municipalities require households to purchase designated garbage bags. The more waste generated, the more bags must be purchased, encouraging waste reduction and recycling.

Why it works: Directly links behaviour with cost.

5. Financial Instruments (Incentives)

🌐 Green Loans for Energy-Efficient Buildings

Banks in several countries offer lower-interest loans for buildings that meet energy efficiency standards. Lower financing costs encourage investment in green technologies.

Example: Green Bonds

Governments and companies issue green bonds to finance renewable energy, sustainable transport, and environmental infrastructure projects.

Why it works: Demonstrates how finance can be directed toward sustainability objectives.

6. Liability Instruments

🌐 Polluter Pays Principle in Hazardous Waste Management

Companies responsible for contamination can be legally required to pay for cleanup and environmental restoration. This encourages firms to prevent pollution before it occurs.

Example: Oil Spill Liability Regimes

Shipping companies and oil operators may be held financially responsible for environmental damage caused by spills.

Why it works: Highlights how legal responsibility influences business behaviour.

7. Performance Bonds and Deposit-Refund Systems

Example: Beverage Container Deposit Systems

Countries such as Germany charge a small deposit on bottles and cans, refunded when containers are returned for recycling.

Example: Mine Rehabilitation Bonds

Mining companies must deposit funds before extraction begins. The money is returned only if the site is restored after mining operations cease.

Why it works: Demonstrates both consumer-level and industry-level applications.